Quote of the Week

“California can make a significant contribution to advancing the cause of dealing with climate change, irrespective of what goes on in Washington. I wouldn’t underestimate California’s resolve if everything moves in this extreme climate denial direction. Yes, we will take action.”

California Governor Jerry Brown

Graphic of the Week

Contents

1. Oil and the Global Economy

2. The Middle East & North Africa

3. China

4. Russia

5. Venezuela

6. The Briefs

1. Oil and the Global Economy

Most of the discussion last week focused on the year just past and what 2017 will bring. Oil prices barely moved during the holiday week closing out the year at $53.72 in New York and $56.82. During 2016, however, US futures closed up about 45 percent for the year and London about 52 percent. It was quite the year for the oil industry with prices ranging from $30 to $55 a barrel; the election of fossil-fuel-friendly Donald Trump to the US presidency; and the OPEC/Russia production cut agreement deemed responsible for the record price rebound during the year.

For 2017 and beyond, there seem to be two major issues that will drive the oil markets. First is whether the Trump administration can spark a rebound in US fossil fuel production by cutting back on regulations and allowing more drilling on federally-controlled lands and waters. While there has been much rhetoric, the implementation of reduced regulations may not be as easy as is widely believed. Efforts to revive the coal industry and spark increased drilling are likely to become entangled in the courts for many years and are unlikely to happen unless they make economic sense. While the incoming administration is likely to abandon the numerous environmental lawsuits against the Obama administration, these are likely to be taken up by environmental groups and will continue for many years.

There will be unanticipated downsides for the Trump administration policies. A trade war with Beijing would increase the cost of some $500 million worth of oil drilling pipe and equipment that is imported to support the oil industry each year. Slower Chinese economic growth by itself is likely to reduce the demand for oil and keep a lid on prices. Much of the impetus behind the surge in oil prices into the $100s was the large increases in Beijing’s demand during the recent two decades. Even relaxing sanctions on Russia and allowing Exxon to fully participate in Moscow’s development of Arctic oil would boost production and keep a lid on prices.

The second big issue of the coming year is how all the myriad factors surrounding the OPEC/Russia oil production cut will net out. First is the question of how much of the 1.8 million b/d production cut that is supposed to start this week will actually happen. Numerous oil ministers have been reassuring us all week that there is clear sailing ahead. However, many have doubts that production will be cut as much as planned, that prices will go up more than enough to offset the revenue loss from the cuts, and that healthy economic growth for the oil exporters will resume. In the past, OPEC cuts have usually resulted in about 60 percent compliance.

Then there is the question of the three OPEC members who have been excused from the cuts due to internal problems. Libyan production is currently around 600,000 b/d. Its National Oil Company is still talking about increasing its production to 1.1 million b/d sometime this year. Before the uprising, Libyan production was around 1.6 million b/d so if the various factions in Libya can suspend their mutual animosities for the common good an increase to above 1 million b/d is not beyond reason. We could see another 500,000 b/d being exported from Libya during the coming year. Nigerian production is currently about 300,000 b/d below normal due to sabotage of its production facilities. The situation, however, has been quiet for the past month, so an increase in production of another 300,000 b/d would be easy to accomplish if the insurgents can be bought off. Oil companies working in Nigeria are making an effort to move new production offshore where it is more difficult to sabotage.

The course of Iran’s production in the coming year is harder to judge. Following the lifting of the sanctions the Iranians were able to increase production much faster than was believed possible, but in recent months this surge seems to have slowed. While several foreign oil companies have made agreements with Iran to explore joint production, so far none of these agreements seem to involve the large amounts of foreign investment necessary to increase Iran’s oil production substantially. Tehran is supposed to be under some version of production ceiling under the OPEC agreement, which allows for some vague increase in Iran’s production.

On the other side of the ledger is Venezuela, which currently seems to be producing oil on the order of 2 million b/d or less. The country is heading to a complete social and economic collapse in the coming year. How much of its oil exports can continue in the coming chaos is an open question. If Venezuelan exports stop completely, it will result in a larger drop in global oil production than is likely under the OPEC agreement. US refineries along the Gulf Coast currently are reporting a large increase in exports of finished products to Latin America. Some of this is said to be replacing oil products that used to come from Venezuela suggesting that Venezuela’s export problems are well under way.

The last question is how much of an increase in US shale oil production will take place in the coming year. The US shale oil rig count continues to climb as oil prices make their way into the $50s. Analysts are estimating that prices will average about $58 a barrel in 2017 – very close to what some claim is now the breakeven point of $60 a barrel in many shale oil locations. The US currently is pumping out about 8.8 million b/d which is about the same as it was producing two years ago; however, this is to be accomplished with only about a third of the drilling rigs that were operational in 2014. Since last May US drillers have added over 200 additional rigs to the count. Some of the higher productivity has come for “efficiencies,” which means drillers are paying workers and service providers much less than they did at the height of the oil boom. An unknown part of these “efficiencies” comes from improving technology that the industry likes to talk about. Outside observers are skeptical that recent technical improvements are adding that much. The key facet of the “more-oil-with-fewer rigs” phenomenon is that nearly all new drilling is taking place in the most productive “sweet spots.”

For the short term, drilling in the most productive places is an effective strategy; however, in a few years, it is likely that there will be few available sweet spots and that the long decline of less oil per well and higher costs of production will set in. For now, it is not clear just what is going to happen to US shale oil production this year. The EIA is forecasting a drop in production, but other observers are saying that it could increase from 500,000 to 1 million b/d, especially if oil prices climb above $60 a barrel for a lengthy period.

In recent weeks, however, there have been reports of a resurgence in the US shale oil industry. Many companies have emerged from bankruptcy with clean balance sheets and the ability to borrow again in hopes that the next round of shale oil production will be more profitable. Some are saying that shale oil producers will increase capital investments by 30 percent this year. As prices move higher, the value of oil reserves to borrow against is increasing. While this is not happening anywhere near as fast as five years ago, we could see an increase in US production.

Oil prices this year will be the net of many factors including Chinese demand, the ever growing renewables industry, and the state of the global economy.

2. The Middle East & North Africa

Iran: The managing director of Iran’s National Oil Company said last week that Tehran expects to award roughly a dozen new agreements for oil and gas development in coming weeks. Whether there is much capital investment coming with these contracts remains to been seen. The director also claimed that producing oil and gas in Iran is much cheaper than in other countries. This may be true as Iran still has large reserves of onshore easy-to-recover oil that have not been produced before due to the string of wars and geopolitical conflicts the Islamic Republic has been involved in since its founding.

Iran’s exports to its top Asian buyers – China, India, South Korea, and Japan – have more than doubled since this time last year. Ship tracking data shows that shipments to these countries in November was just short of the 2016 peak of 1.99 million b/d hit in October.

Tehran says it sealed its deal to buy 80 new Boeing airliners for half of list price. Boeing says the deal is worth 16.6 billion giving pause to the Trump administration’s talk of scrapping the nuclear agreement with Iran. Tehran also plans to buy some 100 Airbus planes from the EU and 20 light turboprops from Italy’s ATR.

Bloomberg notes that the non-oil parts of the Saudi economy are taking a severe hit due to the austerity drive. For the last three years, the government has been balancing the budget by taking money from its sovereign wealth fund which is now significantly smaller. The New York Times reports that despite a cut of $250 billion in non-essential spending, work continues on a mammoth new palace for King Salman on Morocco’s Atlantic Coast.

Syria/Iraq: The Russian-Turkish backed ceasefire in Turkey generally is holding as Baghdad continues its efforts to capture Mosel from ISIL. Over the weekend, Baghdad was hit by a series of ISIL suicide bomber attacks killing about 25.

Iraq’s oil minister told the Kuwaiti news service last week that Baghdad is committed to cutting as much as 210,000 b/d from its January production. A cut of this size will take some time to verify.

Saudi Arabia: Questions are being raised as to whether Riyadh will go through with its plans to sell 5 percent of Saudi Aramco for some $100 billion thereby easing the 2016 government deficit of about $79 billion. Some are asking how much revenue Aramco actually makes as most of its revenue goes to the government in the form of taxes and royalties. To go public, the Saudis would have to open the books and show prospective purchasers of shares in Aramco just how much they would receive in dividends. With the price of oil rebounding sharply due to the prospective production freeze, the Saudis may not be as willing to reveal the details of Aramco’s operations to the world.

3. China

The air quality issue continues to dominate the China’s energy situation this winter. For the second time in a month, very dangerous smog has settled in over Beijing and some 20 other northeastern cities, forcing the closure of schools, factories, and construction sites in addition to cutting vehicular traffic in half. On Sunday the air quality in Beijing was over 500 micrograms of PM 2.5 per cubic meter which is above the top of the scale. Hazardous conditions start at 300 micrograms. For several years now, Beijing has recognized that it faces an existential pollution problem, and has taken many measures to abate the problem. The heart of the issue is maintaining an acceptable level of economic growth while reducing smog-producing sources of energy. While progress is being made, actions up to now are clearly insufficient as the winter air quality continues to get worse reducing the lifespans for millions of Chinese.

Some cities in China have already banned the use of gasoline powered bicycles, scooters, and China’s ubiquitous powered trikes. Some are saying that it is not long until all gasoline and diesel powered vehicles are banned in cities to be replaced by electric vehicles. It is important to remember that China’s primary concern is particulate matter in its air. The impact of carbon emissions is only of secondary concern. Beijing has a large program to convert coal into gas that would then be piped to cities. This plan could lead to major improvements in urban air quality while releasing still more carbon as a byproduct of the conversion process.

Last week Beijing announced that it plans to cap total primary energy consumption at 4.4 billion tons of coal equivalent in 2017. This number is only slightly above the 4.36 billion tons consumed in 2016, which in turn was up 1.4 percent from 2015. From 2005 to 2012, the average annual energy demand growth was 6.4 percent, so maintaining economic growth while keeping energy consumption almost frozen in 2017 is quite a challenge. Another goal is to reduce coal consumption to 60 percent of the total energy consumed from 64 percent in 2015. Non-fossil fuels are to increase to 14.3 percent of total energy consumption from an estimated 13.3 percent this year. The use of natural gas is planned to increase to 6.8 percent of total energy consumption from 5.9 percent in 2015. While China’s energy consumption is to continue growing in 2017, the use of particulate-producing fossils should be slightly lower. However, if the deadly smogs continue to engulf much of China’s urban population each winter more radical measures will be necessary that may even reduce the demand for oil in the years ahead.

Beijing has cut oil product export quotas for the major oil companies by 40 percent in the first round of 2017 licenses. Small refiners called “teapots” seem to have lost their recently acquired licenses altogether. The move came as a surprise to observers who had been expecting increased oil product exports from China in 2017 in line with the major jump in oil product exports seen in recent years. The move may only be a part of an export strategy to deal with saturated oil product markets in Asia. There will be additional rounds of licenses issued in the coming year which may key exports to the size of actual demand.

The Sanmen nuclear reactor project by the Westinghouse division of Toshiba is in a lot of trouble. The project is supposed to be the first of a new series of reactors which is supposed to revolutionize the nuclear industry by being safer, less labor intensive, and quicker to build. The project is years behind schedule as are other projects using the same series reactors. Toshiba stands to lose billions of dollars on the new reactor project.

4. Russia

Russian officials are optimistic that the production freeze and the recent jump in oil prices will be a big help to its economy. Moscow’s finance minister said last week that although Russia’s economy will contract during 2016 and is only forecast to grow by 0.6 percent in 2017, the 2017 forecast now appears to be an underestimate. He believes the economy may grow as much as 1.2 percent this year, if, of course, oil prices remain close to $60 a barrel.

Although President Putin has said the Moscow would abide by the production cut agreement, oil production continued to rise through December. Gazprom-Neft said last week that is production for 2016 is expected to be 650 million barrels or 7.7 percent higher than in 2015. Despite the assurances from Putin, some officials are still hinting that Russia will not jump right into production cutting and lower output may take longer to happen.

Gazprom said it will provide a loan of up to $320 million to help finance the natural gas pipeline through Turkey that would allow Moscow to export gas to the EU without going through Ukraine. The new pipeline which is similar to the now-abandoned South Stream project would bring gas from Central Asia, under the Black Sea, and across Turkey to markets in the EU.

5. Venezuela

The country continues to sink into utter chaos. The senseless decree by the Maduro government pulling all the 100-bolivar currency notes (worth 2 US cents) from circulation before the new and much larger denominations arrived left much of the country without the means to buy anything including food. The decree now has been revised for a second time so that those old notes still in circulation will be valid until January 20th. In the meantime, the country has been subjected to numerous instances of looting and robberies in at least eight cities as desperate Venezuelans scrounge for food. Murders and vigilante lynching are on the rise. The US has warned all US citizens to get out or stay out of the country.

The most recent development is the revelation that the armed forces that are supposed to be overseeing the distribution of food have turned into food traffickers and are now selling food at inflated prices to starving citizens. Food trafficking the Venezuela has become far more profitable than drugs.

In the meantime, Caracas says it will cut oil production by 95,000 b/d this month in accord with the OPEC agreement. The government says it is producing 2.4 million b/d, but most outside observers put production as less than 2 million. There have not been any reliable production figures lately, but given the chaos engulfing the country, it could already be considerably lower than accepted figures.

6. The Briefs

Offshore Denmark, the lack of a viable economic solution for the largest natural gas field in the Danish North Sea means production will end in late 2018, Maersk Oil said. Maersk said that, even after spending more than $140 million on reinforcing structures associated with production over the past 15 years, safety is becoming a clear factor as the facilities are at the end of their operational life. (12/31)

Russia’s Gazprom said it approved financing of up to $320 million to help build a natural gas pipeline planned through Turkey. Gazprom is looking at Turkey as an alternative to Ukraine, through which most of the Russian gas pipelines run. (12/31)

Kazakh President Nursultan Nazarbayev says the country’s sovereign-wealth fund has the money to help wean the central Asian nation off its dependence on oil revenues and build an economy of entrepreneurs. Since Mr. Nazarbayev created the so-called National Fund in 2000, his government has withdrawn $83 billion from it, according to a Wall Street Journal analysis and corroborated by the International Monetary Fund. The National Fund has a balance of $61 billion as of Nov. 30. (12/26)

Mitsui O.S.K. Lines’ massive $400 million floating liquefied natural gas factory is different from most LNG tankers in that it not only carries LNG, but also turns it back into gaseous fuel avoiding the need for an expensive on-land terminal. Mitsui’s vessel is facing a natural gas market that has evolved rapidly over the last few years as onshore gas supplies have grown, and competition in the LNG space has intensified. At this point, Mitsui’s $400 million-dollar ship has no confirmed jobs for more than a year. (12/26)

Algeria’s state energy producer Sonatrach Group plans to increase output of natural gas and crude oil by 20 percent in the next four years as new projects start up. Algeria is Africa’s biggest natural-gas producer. (12/26)

Italy’s Eni said it continued its track record of success in the Mediterranean Sea by securing two new agreements in an Egyptian auction. Both agreements cover acreage in the shallow waters of the Mediterranean Sea. Eni serves as the operator of the two fields in partnerships that include British energy company BP and French supermajor Total as minority players. (12/29)

Angola is one of the lesser producers in the Organization of Petroleum Exporting Countries, accounting for less than 1 percent of the total output from the group. Oil supports about 45 percent of the nation’s economy and nearly all of its exports. An assessment from the IMF found the decline in crude oil prices since 2014 caused severe damage to the Angolan economy. (12/31)

Mexico’s record-low refinery production and growing consumer demand helped push US gasoline exports there to a new high in October, a trend that has boosted prices in both countries. Gasoline exports to Mexico climbed 1.86 million barrels to 12.08 million barrels in October, the highest total since that data started being tracked in 1993. (12/31)

Mexico will raise gasoline prices by as much as 20 percent in January, stoking inflation that’s already running at the fastest pace in almost two years. A month after the increase is implemented, prices will start to adjust on a daily basis as the government loosens its control of the gasoline market. The jump in prices risks pushing up inflation at a time when a slump in the peso has already fueled concern about rising consumer prices and led the central bank to raise interest rates five times this year. (12/28)

The US oil rig count grew by two last week, according to Baker Hughes Inc. That brings the total count up to 525, the most since December 2015 and 11 less than the 536 rigs seen at the end of 2015. The gas rig count added three rigs amid rapidly rising natural gas prices. (12/31)

2016 bankruptcies: Even as oil prices are rebounding, we are closing out one of the worst years for the oil and gas industry in decades. In 2016, the U.S. oil and gas industry defaulted on $39 billion in high-yield energy debt, more than twice as much as the $15 billion in defaulted debt in 2015, according to Fitch. One in three U.S. oil and gas exploration companies defaulted on high-yield bonds in 2016. (12/30)

Three small U.S. oil companies—Houston’s Memorial Production Partners, Denver’s Bonanza Creek Energy and Forbes Energy Services of Alice TX—will file bankruptcy papers soon as the financial squeeze that led to scores of bankruptcies across the industry continues. More than 200 North American drillers and oil field service companies have been forced into bankruptcy in the two-and-a-half-year oil bust. But analysts believe oil and gas bankruptcies will slow dramatically next year as climbing crude prices ease financial pressure on shale drillers. (12/30)

US refiners exported record amounts of oil products last week, taking market share from struggling competitors in Mexico and the Caribbean. Almost 4 million barrels a day of gasoline, distillates like diesel and heating oil, and propane left the country as refiners in Texas and Louisiana processed the most crude in at least 24 years. Demand has grown this year as competitors in Latin America sputtered out with maintenance issues. (12/30)

US Gulf Coast refiners, after years of running flat out, are lining up repairs to plants in 2017 – but facing a severe labor shortage that could delay work, drive up costs and raise accident risks. Fuel producers such as Marathon Petroleum Corp and Valero Energy Corp have delayed routine work in the past 24 months amid high margins. Those margins collapsed this year in a global fuel supply glut, providing an incentive for refiners to undertake the shutdowns necessary for maintenance. But refiners are now competing for pipe fitters and ironworkers with a host of billion-dollar energy projects. (12/29)

US LNG exports started in February this year. Based on cheap American shale gas, Europe had been expected to see a good proportion of cargoes given the relatively short shipping route and Europe’s massively underused LNG import capacity. But with European gas prices staying stubbornly low for most of the year and the margins for US LNG having been largely eroded due to the slump in global LNG prices, in the end only a handful of cargoes ended up in Europe. As 2016 nears its end, 50+ cargoes have left the Cheniere Energy-operated Sabine Pass terminal in the Gulf of Mexico for international markets. (12/27)

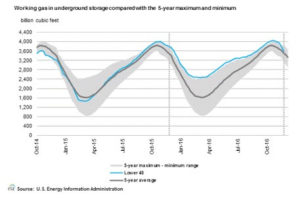

Natural gas prices are surging as cold weather eats into U.S. inventories, tightening the market much more quickly than many analysts had expected. The blast of Arctic weather in December put a strain on natural gas markets, with millions of people cranking up the heat to keep warm. The EIA reported a surprise drop in storage levels in the week ending on December 16, falling by 209 billion cubic feet. That decline puts total storage levels at 3,597 Bcf, or just a small 78 Bcf above the five-year average. (12/28)

In lower Manhattan, the open-outcry trading floor of the New York Mercantile Exchange will shut down after markets close Friday, the latest step in the inexorable shift toward electronic trading. CME Group Inc., which owns the Nymex, said in April that the New York trading floor would close at the end of the year after the share of options volume executed there had dwindled to just 0.3% of the company’s overall energy and metals volumes. Chicago-based CME had already stopped futures trading on the Nymex floor last year. (12/30)

Peabody Energy said on Thursday it extended a deadline for creditors to join financing deals aimed at bringing the largest US coal miner out of bankruptcy amid growing creditor support for its plan of reorganization. Last week, Peabody unveiled its plan to eliminate more than $5 billion of debt and raise capital from creditors with a $750 million private placement and a $750 million rights offering. (12/29)

Solar rising: Thierry Lepercq, head of research, technology and innovation at the French energy company Engie SA, said in an interview at Bloomberg that he sees a potential for the cost of solar electricity to fall below $10-megawatt hour (1¢/kWh) in the sunniest climates by 2025. (12/29) (Note: 1¢/kWh seems like a reach)

Trump vs. CA on climate change: Foreign governments concerned about climate change may soon be spending more time dealing with Sacramento than Washington. President-elect Donald J. Trump has packed his cabinet with nominees who dispute the science of global warming. He has signaled he will withdraw the United States from the Paris climate agreement. He has belittled the notion of global warming and attacked policies intended to combat it. But California — a state that has for 50 years been a leader in environmental advocacy — is about to step unto the breach. In a show of defiance, Gov. Jerry Brown, a Democrat, and legislative leaders said they would work directly with other nations and states to defend and strengthen what were already far and away the most aggressive policies to fight climate change in the nation. (12/28)