Images in this archived article have been removed.

By Steve Andrews.

(Commentaries do not necessarily represent the position of ASPO-USA)

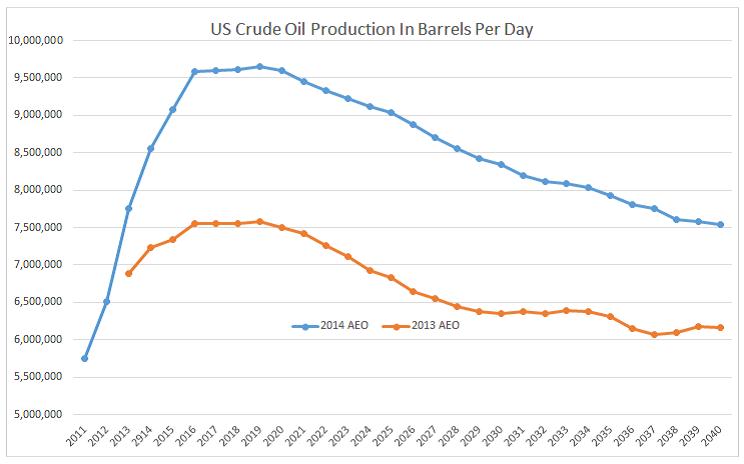

The key take-away from the US EIA’s Annual Energy Outlook released one week ago jumps out in the graph below: US crude oil production should peak in 2016 at a level 26% higher than that projected just one year ago. That’s an additional 2 million barrels a day (mb/d), pushing the US total to 9.6 mb/d within three years—the same total that the US produced during its first peak in 1970, as an acquaintance at the EIA pointed out last week. That’s three more break-through years like the last two. Then flat. Finito. As some wag asked last week, is that really a recipe for a continuing oil revolution or an oil retirement party?

Data: EIA’s Early Release Annual Energy Outlook, 2014. From Ron Patterson.

It would be peachy for the US oil industry and oil consumers both here and abroad if US oil production rocketed to 9.6 million barrels/day by 2016 and held at that level for four years. Through the first nine months of 2013, EIA data for the US already shows average crude production at 7.3 million b/d and rising strongly. So repeating at 9.6 million b/d would seem to be a viable scenario, especially if some new deepwater fields in the Gulf of Mexico kick in within two or three years.

Yet as geologist David Hughes and financial analyst Mark Lewis reported to roughly 40 Trans-Atlantic Energy Security Dialogue attendees two weeks ago, the U.S. industry is battling raging production decline rates, the tailing off of sweet spots in our two largest shale oil plays, the brutal reality of an accelerating drilling treadmill, and relentlessly rising costs.

For those and other reasons, the EIA’s latest projection strikes this writer as being too optimistic. The peak seems too high and the plateau too long. And this just in: EIA apparently now assumes no major increase from their largest-rated shale oil field in the US—their 15 billion barrel Monterey shale, in California’s San Joaquin Valley—over the next couple of decades. That helps cast big-time doubt on EIA’s long-term projection, which assumes just a gradual 100,000 b/yr decline rate for total US crude oil production for 20 years.

But unlike long-range forecasts, we won’t have to wait too long for this one to play out. The beef is front-loaded. So mark down your own most likely scenario. Then put me down for a peak of 8.5 million b/d in 2015-16, plus a three-year “bent plateau” at best. Then keep all three estimates for your dartboard.

But don’t forget the larger picture here: at the world level, the surprising U.S. shale bonanza will most likely slip into decline relatively soon, worldwide shale plays will probably arrive later and bring more modest supply, all this is costing us much more than fuel used to (on multiple levels), and the world’s financial system—on which all oil and gas drilling is based—seems to be ominously creaking in the background. And pricey oil doesn’t help muffle that squeaky financial wheel.

Steve Andrews is a semi-retired energy consultant who edits “The Briefs” herein each week. He has followed the world oil story for three decades.